Since the first Earth Day in 1970, activists across the world have used the occasion to push for an increased awareness of environmental issues and lobby for policy changes. The climax of this year’s event today, the Earth Day Live digital event, will coincide with the Leaders Summit on Climate hosted by Joe Biden’s U.S. Presidential Administration, where world leaders will meet to discuss the need to take stronger action on climate change ahead of the United Nations’ Climate Change Conference this November in Glasgow.

To mark Earth Day 2021, the strategic consultants at IDTechEx provided insight on some of the technologies that they believe will be instrumental in winning the fight against climate change. They say that technology will play a key role in the fight against climate change. The continuing growth of electric vehicles and renewable energy is helping to wean the world off fossil fuels, while emerging fields such as carbon capture, utilization, and storage, and negative emissions technologies could even help reverse decades of emissions.

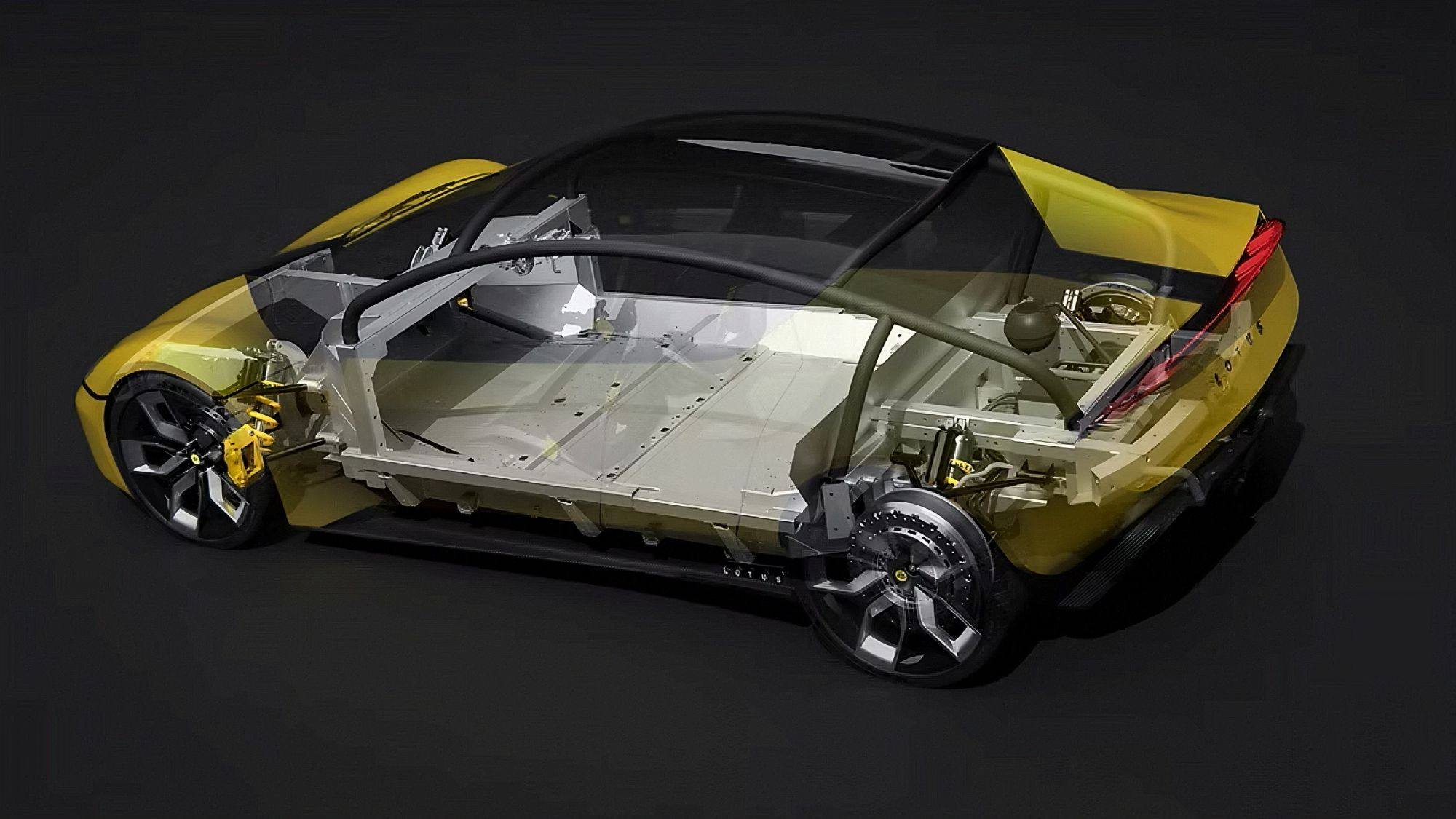

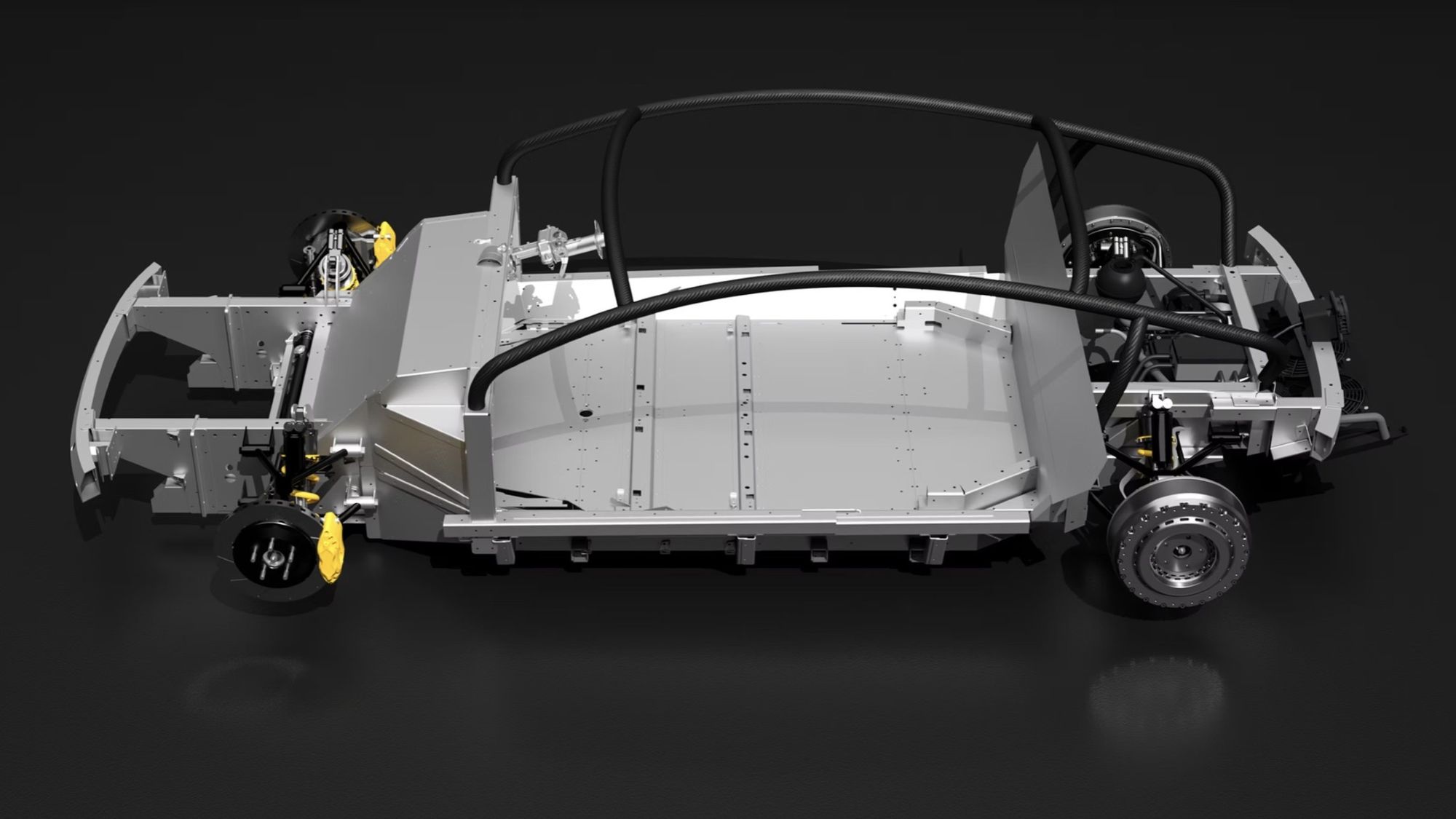

Electric vehicles

Electric car markets soared in 2020, growing over 40% year-on-year, according to IDTechEx’s Advanced Electric Cars 2020-2040 report. The organization expects growth to continue for the next two decades.

The sheer volume of the global car sales—about 78 million in 2020, according to LMC Automotive—means that passenger vehicles account for the lion’s share of CO2 emissions from transportation—about 45% in 2018, according to the IEA (International Energy Agency). As a result, passenger cars are a key part of green transport policy coming into place to address new climate goals.

Often, industrial policy is technology agnostic. However, in practice, battery-electric vehicles offer the lowest-emission solution for the lowest cost in most mobility sectors and are the endgame, say IDTechEx experts.

Much of 2020’s electrified-car growth was driven by Europe, which stuck by a transitional year towards new emissions targets of 95 g of CO2 per km. Sales of plug-in electric cars nearly doubled, rivaling China’s numbers, but those numbers include hybrids as automakers attempted to reach these targets.

Critically, according to IDTechEx, Europe is becoming less dependent on leading innovator Tesla as traditional automakers have ramped up their electrification plans. Ford, Hyundai and Kia, JLR, and VW all made upward revisions to their targets in the first few months of 2021. Their efforts are paying off, as VW recently took the European top spot from Tesla in terms of unit sales, following the success of the e-Up, a short-range (161-mi WLTP range) city car.

Similar policies are taking shape around the world. China is transitioning away from purchase subsidies and towards a “double credit” scheme, which fines automakers for not selling enough of what it defines as a “new energy vehicle”—a battery-electric, plug-in hybrid, or fuel cell vehicle. In the U.S., the Biden Administration also has plans to revise emissions targets.

The net effects are industrial policies from around the world will push battery-electric vehicles into the mainstream this decade.

Sustainable fuels

Coupled with the integration of renewable power sources, electrification offers the most efficient route to decarbonization. However, not all industries will be able to completely electrify, say IDTechEx researchers.

Aviation presents the most obvious example where electrification and battery technology are unlikely to provide a viable solution for much of the industry. Here, fuels are likely to be needed for the foreseeable future, and sustainable aviation fuels (SAFs) continued to garner interest over the past year. Most recently, United Airlines announced a partnership with corporate customers to purchase 3.4 million gallons during 2021, while Total began production of SAF at a biorefinery in France, responding to French government targets for SAF consumption.

SAFs make use of sustainable feedstocks and, compared to conventional jet fuels, can offer up to an 80% reduction in CO2 emissions. Today, feedstocks are biogenic, meaning SAFs are biofuels. While there are multiple routes to producing SAFs, the vast majority of production capacity is for the production of hydro-processed esters and fatty acids (HEFA-SPK). IDTechEx estimates that by 2025, over 85% of SAF production capacity will be for HEFA-SPK. The process uses vegetable or waste oils, such as used cooking oil, as feedstocks.

Synthetic e-fuels offer an alternative to biofuels, mitigating concerns over the sustainability of biofuel feedstocks. E-fuels combine H2, produced from water electrolysis, with a source of carbon, such as from direct-air-capture, to produce intermediates such as methanol and syngas—and eventually drop-in fuels. Norsk E-fuel, a collaboration between electrolyzer company Sunfire and direct-air-capture company Climeworks, is aiming to have a pilot plant operational by 2023 capable of producing 10 million liters of renewable e-fuels.

The key issue with e-fuels is cost, as both electrolyzer and carbon-capture technology are expensive. Further, economic production will be reliant on the use of low-cost electricity, meaning the electrolyzer will have to operate dynamically to make use of excess and low-cost electricity. Dynamic operation is something electrolyzers are generally not well suited to and given high capital costs, they would ideally need to be operated almost continuously rather than dynamically. Ultimately, the market for e-fuels is very much in its infancy and improvements to electrolyzer and carbon capture technology are likely needed for commercially viable e-fuel production.

Other technologies

The IDTechEx researchers also highlighted stationary energy storage and CCUS (carbon capture, utilization, and storage) as promising technologies.

The past 10 years have seen considerable growth in the installation of solar PV (photovoltaic) and wind power onto electrical power grids. However, as the penetration of variable renewable power sources increases, so too does the difficulty of continuously matching supply and demand over various time frames. Energy storage is set to play a key role in maintaining grid stability and in helping to make renewable power sources dispatchable.

Apart from pumped hydropower, the dominant stationary energy storage technology of today is the Li-ion battery, its development and deployment having benefitted from the scale of the automotive industry. The takeaway is that there are a variety of performance characteristics that are needed for stationary applications, and with battery technology unlikely to be economically feasible for long-duration storage, there will be a myriad of energy storage technologies deployed over the next 10 years to help incorporate increasing levels of renewable power.

CCUS, or CCS (carbon capture and storage), is a set of technologies used to strip carbon dioxide from industrial waste gases or directly from the atmosphere. Once the carbon dioxide is captured, it is either stored permanently underground (carbon storage) or it is used for a range of industrial applications (carbon utilization), such as CO2-derived fuels or building materials. CCUS technologies are likely to play a key role in the fight against climate change, with the UN estimating that CCUS could mitigate between 1.5 and 6.3 Gt of CO2 equivalents per year by 2050.

Using CO2 that would have otherwise been released as emissions can help mitigate climate change. However, using CO2 in products or services does not necessarily reduce overall emissions in the long term. Quantifying the potential climate benefits associated with and CO2 utilization pathway is complex and challenging and may require a life cycle approach. The climate benefits associated with CO2 use primarily arise from displacing a product or service that has higher life-cycle CO2 emissions, such as fossil-based fuels, chemicals, or conventional building materials.

For more info on any of these technologies, visit www.IDTechEx.com.

{kind=link}